What is methane pyrolysis?

Methane pyrolysis, also known as methane cracking or turquoise hydrogen, is the high-temperature breakdown of methane into hydrogen gas and carbon. It competes directly with blue hydrogen, hydrogen from steam methane reforming and carbon capture and sequestration (CCS), to produce low-carbon hydrogen from natural gas. In methane pyrolysis, all the carbon content in the methane is captured in solid form rather than emitted as carbon dioxide.

Types of methane pyrolysis technologies

Methane pyrolysis requires approximately half the amount of energy required by steam reforming to produce the same amount of hydrogen. Finally, the solid carbon byproduct can be sold as carbon black, offsetting the cost of hydrogen produced. Together, these factors make methane pyrolysis a promising technology option to produce low-carbon hydrogen.

Methane pyrolysis takes different forms, and they can be categorized as plasma, catalytic, and thermal. Despite the variations, they all share common technical challenges: high process temperatures required for high conversion rates, hydrogen gas purity, and separation of solid carbon from the gas phase to avoid catalyst poisoning (if any) and reactor system clogging due to the solid carbon. To provide a comprehensive overview of the technology landscape for methane pyrolysis among the different players and regions, we analyzed locations and developers of all sizes [corporate and small to midsize enterprise (SME)] across all geographies (Americas, APAC, EMEA) using Lux’s proprietary data tools. This information defines future trends and, more importantly, helps identify opportunities for clients seeking to engage with players in methane pyrolysis.

Landscape of Methane Pyrolysis

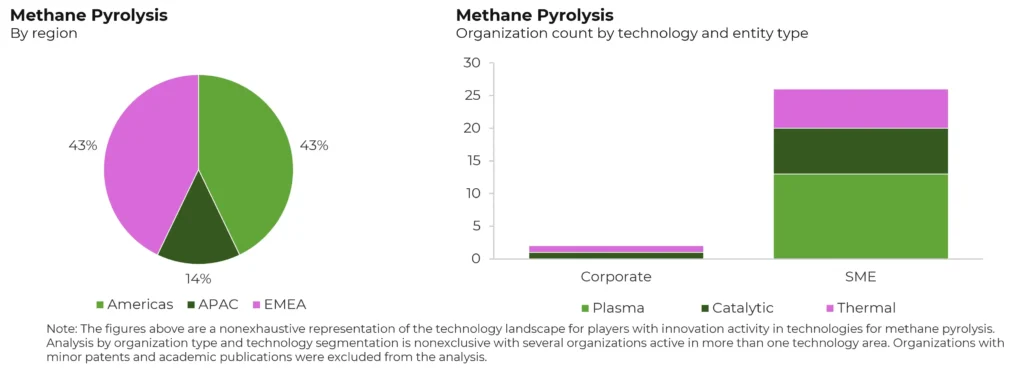

Americas lead the methane pyrolysis landscape, followed by EMEA

About 44% of methane pyrolysis technology developers are based in the U.S. or Canada, where the feedstock price is cheaper than in Europe and Asia. The attitude toward repurposing existing assets in North America is also more favorable than in other regions, considering that the only operational commercial methane pyrolysis facility is located in the U.S., and the second one is being planned in Canada. SME activity in EMEA is driven by companies based in the EU. Despite high SME activity, the EU doesn’t have the right market conditions to foster the deployment of methane pyrolysis facilities in the region; these companies will either need to expand into the favorable American market like the Finnish company Hycamite is planning with NW Natural to build its next plants in the U.S. or secure access to government grants.

SMEs dominate the space

There are 25 SMEs developing differentiated methane pyrolysis technologies, and the majority are at lab or R&D scale with plans to deploy pilot-scale units by 2025. Project development agreements with major corporations that are interested in both hydrogen and solid carbon will put companies ahead of their competitors; however, companies today mostly find themselves lacking solid carbon offtakers.

Plasma pyrolysis has the highest number of players

Most organizations in methane pyrolysis are developing plasma pyrolysis technology as it is currently the only methane pyrolysis technology proven at scale; however, there is no corporate activity in plasma pyrolysis. Thermal and catalytic pyrolysis have a similar number of players with an equal number of corporations. The high number of plasma players does not directly guarantee commercial success — most will struggle to find project partners due to the plasma’s high energy intensity. Catalytic and thermal pyrolysis platforms will exhibit higher momentum as they have over the past couple of years.

Methane pyrolysis technology breakdown:

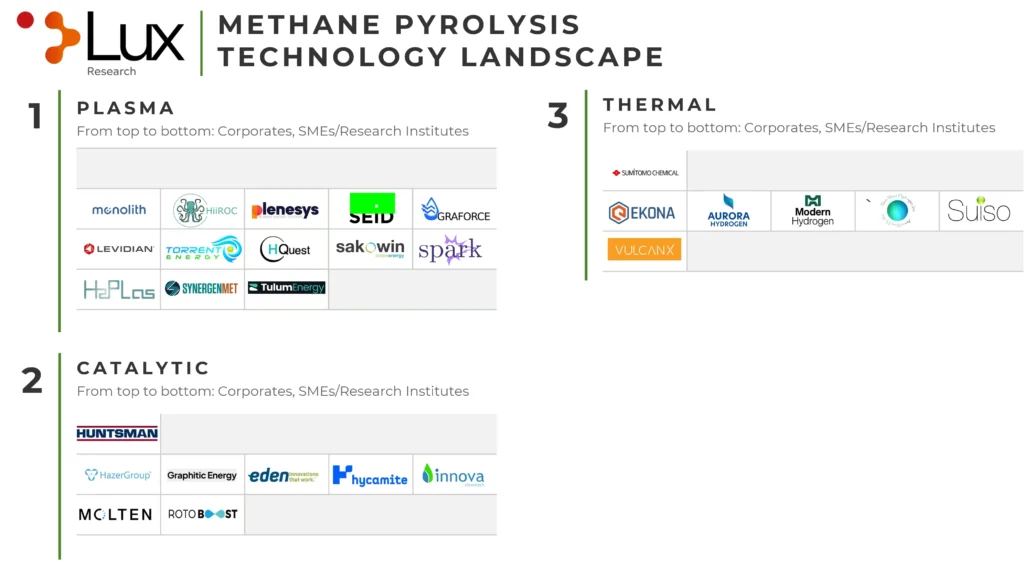

Plasma

Plasma pyrolysis is the most mature form of methane pyrolysis, using a plasma torch to decompose methane at temperatures between 1,000 °C (cold plasma) and 2,000 °C (hot plasma). Cold plasma typically achieves less than 50% methane conversion without catalysts, while hot plasma exceeds 90%. However, hot plasma demands significant electricity (~25–30 kWh/kg H2), prompting companies to focus on improving cold plasma performance, which consumes less than 15 kWh/kg H2. Among all methane pyrolysis routes, plasma has reached the highest technology readiness level and currently represents the most advanced option. Monolith Materials leads in plasma pyrolysis, deploying hot plasma at its first U.S. demonstration facility launched in 2020. The facility outputs carbon black as the main product, consuming about 25 kWh/kg H2 in addition to natural gas feedstock. It currently produces 14,000 tonne/y of carbon black and 4,500 tonne/y of H2. Monolith planned a more than 10× capacity expansion with Olive Creek II by 2025, but has not released public updates. Other plasma pyrolysis players include HiiROC (hot plasma) and Graforce (cold plasma). HiiROC partnered with ABP and px Group on a 10-tonne/day hydrogen project at Saltend Chemicals Park in the U.K. Graforce is expanding in APAC and Brazil after deploying its first reactor in Austria, through partnerships with Worley, Sanepar and Plantec. Plenesys and Levidian are also advancing commercialization. In Australia, Turquoise Group began constructing a commercial plasma methane pyrolysis plant using Plenesys’ HyPlasma technology. Levidian is expanding its footprint in Southeast Asia and the Middle East through new partnerships.

Catalytic

In catalytic pyrolysis, methane decomposes into hydrogen and carbon over a metal catalyst at 600 °C–900 °C. The process typically uses packed or fluidized bed reactors, with iron, nickel, and cobalt as the most studied catalysts due to their abundance and lower cost compared to noble metals. Nickel offers the highest catalytic activity but deactivates above 600 °C. Cobalt-based catalysts also perform well but are more expensive and toxic, requiring additional steps to purify the resulting carbon black. Iron-based catalysts, by contrast, are inexpensive, nontoxic, and offer more stable performance. Although catalysts reduce the activation energy required to initiate pyrolysis, rapid deactivation and the need for regeneration at operating temperatures remain key barriers to commercialization. Carbonaceous catalysts can avoid regeneration but suffer from declining activity over time. Catalyst selection and the nature of the carbon byproduct differentiate catalytic pyrolysis approaches. Since the operating temperatures are too low to form carbon black, developers tailor catalysts to produce alternative materials such as graphite or carbon nanotubes. This technology remains in early development. Hazer Group and Hycamite are leading efforts in this space. Hazer Group uses a fluidized bed reactor with an iron ore catalyst operating at 900 °C. Its process consumes an estimated 10–20 kWh/kg H2 and currently runs at pilot scale, with two commercial plants planned to deliver 2,500 tonne/y of H2. Hazer plans to deploy one facility in Canada in collaboration with Suncor and FortisBC and the other in France as part of its extended partnership with Engie. Hycamite is constructing a 2,000-tonne/y hydrogen plant in Finland, which will be Europe’s largest. Graphitic Energy (formerly C-Zero) pivoted in late 2024 from a molten metal/salt process and launched a 400-kg/day H2 pilot plant in Texas.

Thermal

Thermal, or hot, pyrolysis breaks down methane into hydrogen and carbon at temperatures above 1,200 °C without catalysts. The process struggles at temperatures below 1,000 °C due to prolonged cracking times but achieves high conversion rates under low pressure and high temperature. At low pressures, intermediates such as olefins and aromatics form and decompose into hydrogen and carbon as residence time increases. The primary differentiator in thermal pyrolysis lies in the energy source used to generate the required heat. The simplest method — burning natural gas — raises concerns about the carbon intensity of turquoise hydrogen. To address this, some companies, including Modern Hydrogen, divert up to 25% of their hydrogen output to generate low-carbon heat. Modern Hydrogen is running a pilot demonstration with NW Natural in Oregon. Ekona Power is constructing a 1-tonne/day turquoise hydrogen facility with ARC Resources in Canada. Meanwhile, other developers are pursuing microwave-based heating as a cleaner alternative. Sumitomo Chemical remains the only corporation developing microwave-assisted methane pyrolysis, currently at lab scale, with plans to commercialize by the early 2030s. Aurora Hydrogen, an Alberta-based startup, is also advancing microwave-based technology. It raised USD 10 million to scale up to a 200-kg/day pilot and claims an energy requirement of 35 MJ (9.7 kWh)/kg of H2, excluding feedstock. At an earlier stage, New Wave Hydrogen is developing shockwave-compression heating. The lab-scale company reports an energy use of 2.3–5.4 kWh/kg H2. VulcanX is pursuing a heat-source-agnostic approach using molten aluminum. It operates a 200-kg/day hydrogen pilot in Alberta with ATCO, although it has not disclosed utilization rates.

Methane pyrolysis has gained interest over the past several years as an alternative approach for producing low-carbon hydrogen from natural gas, along with a solid carbon product that is easier to handle than CO2 and can be sold on the market. However, the commercial prospects of the technology have been limited by the finite carbon offtake market to achieve cost parity with its direct competitor, blue hydrogen. Most companies in methane pyrolysis claim to be capable of competing on cost with blue hydrogen without selling carbon byproducts; however, these claims are not validated at scale.

The Lux Take

Commercial availability of methane pyrolysis will depend on the demand for solid carbon as well as favorable policies. Clients should keep an eye on the additive markets (concrete, asphalt, tire manufacturing, etc.) in the near term and performance markets (batteries, graphite electrodes, electronics, semiconductors) in the long term. Policies like the EU’s delegated regulation, which does not count solid carbon as emitted if embedded or permanently stored, could also accelerate deployment in certain regions within the EU without geological CO2 sequestration sites if the demand from additive markets picks up.

Curious for more information on these key players? Learn more from our analysts.